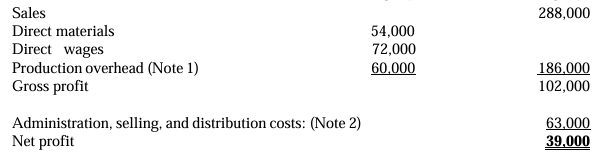

Question

a) Claudia Footwear (CFW) has developed a new range of high-quality affordable sandals for beachwear. The sandals are based on an innovative design that protects feet from the effects of sun, salt, and sand. The company has already received some sales orders for 9,000 sandals which form 75% of the operating capacity of CFW, and production is due to commence next month. The Management Accountant has prepared the following projections based on 75% operating capacity for the trading year ahead:

Notes:

- Production overhead is made up of fixed and variable costs in the proportion of 7:3, respectively.

- GH¢36,000 of the total administration, selling, and distribution costs is fixed, and the remainder varies with sales volume.

Required:

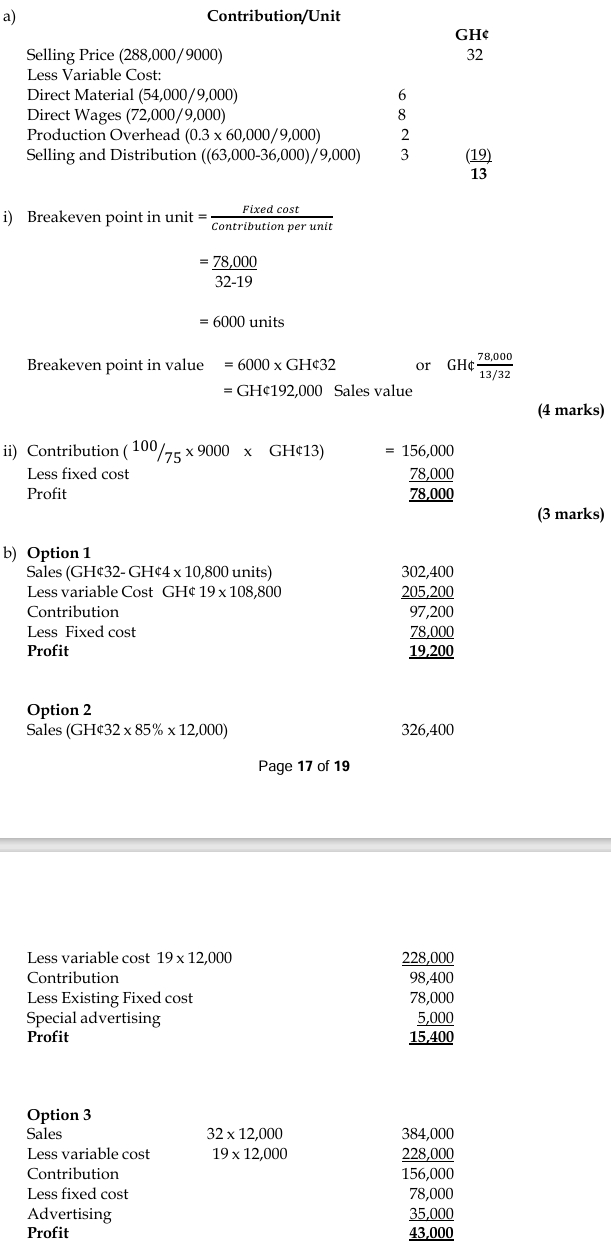

i) Calculate the breakeven point in units and value. (4 marks)

ii) Calculate the profit that could be expected if the company operated at full capacity. (3 marks)

b) In order to enhance profitability, CFW has proposed the following options:

Option one:

If the selling price per unit were reduced by GH¢4, the increase in demand would utilize 90% of the company’s capacity without any additional advertising expenditure.

Option two:

To attract sufficient demand to utilize full capacity would require a 15% reduction in the current selling price. In addition, however, CFW would have to spend GH¢5,000 on a special advertising campaign.

Option three:

To attract sufficient demand to utilize full operating capacity without changing the selling price per unit, CFW has to spend GH¢35,000 on a special advertising campaign.

Required:

Present a statement showing the effect of the three alternatives compared with the original budget and advise management of CFW which of the FOUR possible plans ought to be adopted (the original budget plan or any of the three options). (10 marks)

c) State TWO (2) limitations and ONE (1) usefulness of Cost-Volume-Profit analysis. (3 marks)

Answer

Recommendation:

Based on the analysis, Option 3 should be adopted as it results in the highest profit of GH¢43,000. (10 marks)

c) Limitations and Usefulness of CVP Analysis:

Limitations:

- Assumption of Constant Fixed Costs:

CVP analysis assumes that fixed costs remain constant, which may not be realistic as fixed costs can change with scale or over time. (1 mark) - Assumption of Constant Variable Costs:

It assumes that variable costs per unit remain constant, but in reality, economies of scale or other factors can cause variable costs to fluctuate. (1 mark)

Usefulness:

- Decision-Making Tool:

CVP analysis is useful for managers as it helps in understanding the relationship between costs, volume, and profit, and aids in making informed pricing, production, and investment decisions. (1 mark)

(3 marks)