Question

Answer

a)

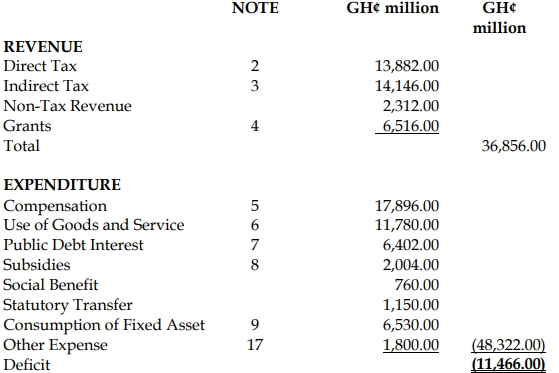

CONSOLIDATED FUND OF GHANA

STATEMENT OF FINANCIAL PERFORMANCE FOR THE YEAR

ENDED 31/12/2020

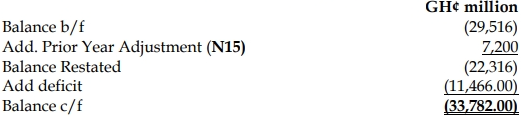

Statement of Accumulated Fund for the year ended 31/12/2020

b)

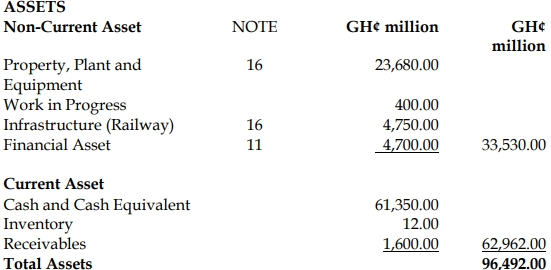

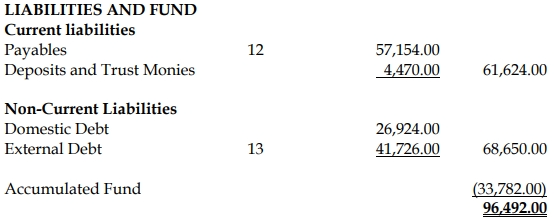

CONSOLIDATED FUND

STATEMENT OF FINANCIAL POSITION AS AT 31/12/2020

c) Conditions for Revenue Recognition (IPSAS 9):

Revenue from the sale of goods shall be recognised when all the following conditions have been satisfied:

- The entity has transferred to the purchaser the significant risks and rewards of ownership of the goods.

- The entity retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold.

- The amount of revenue can be measured reliably.

- The economic benefits or service potential associated with the transaction will probably flow to the entity.

- The costs incurred or to be incurred in respect of the transaction can be measured reliably.