Question

You are a manager in BS Cipax, a medium-sized firm which offers a range of services to audit and non-audit clients. You have been asked to consider a potential engagement to review and provide a report on the prospective financial information of Filtane Limited, a company which has been an audit client of BS Cipax for six years. The audit of the financial statements for the year ended 31 August 2015 has been completed and your firm issued an unmodified report. Filtane Limited operates a chain of fashion stores across the country.

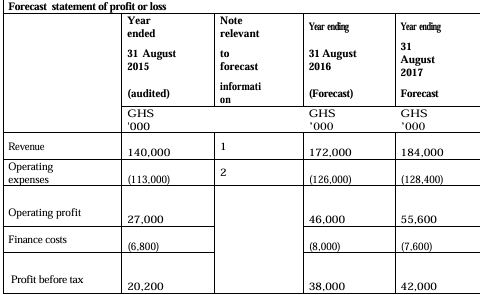

Currently its merchandise are out of date and it sells clothing which do not reflect the latest and in mode fashion labels which are becoming more popular especially with the youth. Management is planning to revamp its image and stock the latest fashion in Africa and across the other continents. It also intends to invest in the latest technologies to include online real time trading on the internet order to attract more customers, especially the up-and-coming youth, trendy middle-aged persons and even those far from its shops by attracting them to shop over the internet. The company has sufficient cash to fund half of the necessary capital expenditure, and has approached its bank, Boafo Bank Limited, with a loan application of GHS32 million for the remainder of the funds required. Most of the cash will be used to invest in acquiring inventory and the technology for ensuring secure and safe online trading. The remaining cash will be used for refurbishment of the shops. Management had informed the Audit team, in the invitation to start the audit, of its intention to use the audited financial statements as the basis for preparing the prospective financial information to be used to seek for the loan from Boafo Bank Limited. The draft forecast statements of profit or loss for the years ending 31 August 2016 and 2017 are shown below, along with the key assumptions which have been used in their preparation. The audited statement of profit or loss for the year ended 31 August 2015 is also shown below.

The forecast has been prepared for use by the bank in making its lending decision, and was to be accompanied by other prospective financial information including a forecast statement of cash flows. Note 1: The forecast increase in revenue is based on the following assumptions:

(i) All shops will be stocked with new modern and in mode fashion to attract new customers to the shops and many persons who don’t live in the vicinity of the shops will also be attracted through online shopping by December, 2015.

(ii) Prices will increase by an average of 25% in December 2015.

Note 2: Operating expenses include mainly staff costs, depreciation of property and fittings, and repairs and maintenance to the shop fittings and equipment as well as ensuring continuous safe and secure on-line shopping.

Required:

a) i) Explain the matters to be considered by BS Cipax before accepting the engagement to review and report on the prospective financial information of Filtane Limited. (5 marks)

ii) Assuming the engagement is accepted, and the results of the examination procedures show that the prospective financial information have been prepared in accordance with the assumptions and appear reasonable, discuss the issues that will be in the report your firm will issue in respect of the forecast statement of profit or loss. (8 marks)

b) Boafo Bank Limited gave the loan to Filtane Limited on 15 October 2015, and a review of the first six months of operation in May 2016 of the new shops revealed that the company was not doing well and could not pay the first installment for the loan from Boafo Bank Limited. Further investigation revealed that the audited financial statements signed by BS Cipax, which showed a profit of GHS20.2M, should have been of a loss of GHS4.3M.

Boafo Bank Limited has indicated its intention to sue your firm for negligence on the basis that it placed reliance on the financial statements audited by your firm.

Required:

Comment on the matters that you should consider in deciding whether your firm will contest the matter in court or seek an out-of-court settlement with the bank. (7 marks)