Question

Answer

a) Distinction between Market Price and Value (3 marks):

Price:

- Price is determined by the market forces and is obtained by the interplay of demand and supply.

- Price is the amount that a willing buyer is ready to pay, and a willing seller is prepared to accept for the exchange of an item.

- Price is always expressed in monetary terms except in the case of barter where the price of a commodity is quoted in reference to the quantity of another commodity.

- The price of an asset can also be determined as the present value of all future cash flows of the stated asset.

- Price can be higher than the value of an item when a premium is paid or lower when a discount is granted.

Value:

- Value, on the other hand, is the allocation of monetary worth to an item or a subject of valuation.

- Unlike price, value can be tangible or intangible.

- Everything has a value, which may be different from the price; though the price can be used as a measure of the value of an item.

- Whereas price is agreed upon and fixed between a buyer and a seller for a given item, the value of the item in question may differ among the parties.

- Processes to establish a common value of an item is often the starting point to determine the price.

b) Why Valuation Process is Described as Subjective (2 marks):

- Valuation methods apply several assumptions that may vary in the future.

- Different methods produce different values, which can create disagreement on the appropriate method to apply.

- Several elements for the valuation are based on estimation (future cash flow), which may vary materially from the actual results.

- Different perspectives of interested parties influence their choice of valuation method. For instance, valuation for taxation purposes may consider factors for the computation of capital gain, which may be different from valuation for accessing credit facility, which will focus on collateral value.

- Some methods, such as the discounted cash flow, have been described as subjective.

- The quality of information and completeness thereof influence the competence of the valuation process.

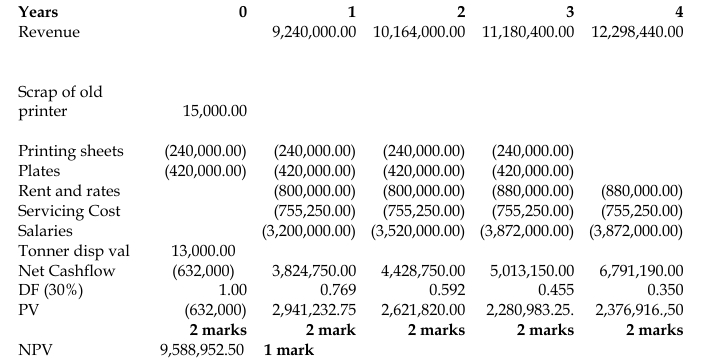

c) Discounted Cash Flow Valuation (12 marks):

d) Assets-Based Valuation (3 marks):

| Item | Value (GHS) |

|---|---|

| Equipment (NBV) (8,000,000/6 × 4) | 5,333,333 |

| Scrap value of old printer | 15,000 |

| Scrap value of tonners | 13,000 |

| Stock of replacement parts | 300,000 |

| Printing sheets | 240,000 |

| Plates | 420,000 |

| Total Valuation Amount | 6,321,333 |