Question

Answer

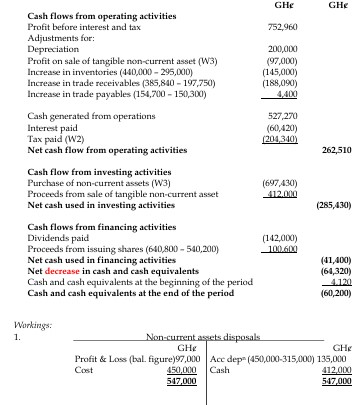

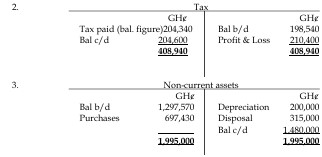

a) Oti Ltd: Statement of Cash Flows for the year ended 31 March 2022

b) Cash Equivalents:

Cash equivalents are short-term, highly liquid investments that are readily convertible into known amounts of cash and that are subject to an insignificant amount of risk of changes in value. An investment normally qualifies as a cash equivalent only if it has a short maturity, say, three months or less, from the date of acquisition.