Question

a) Distinguish between capital expenditure and revenue expenditure. (5 marks)

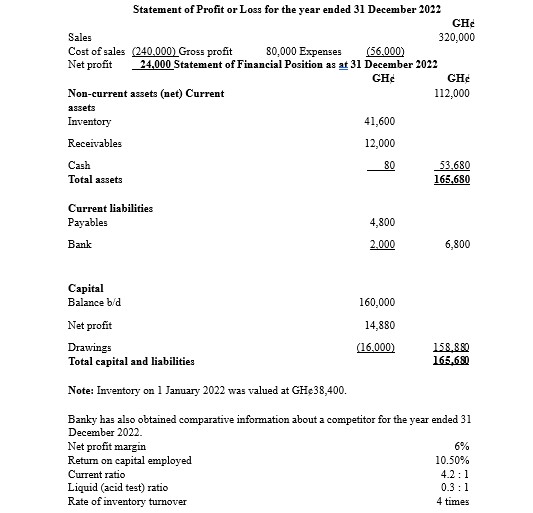

b) Banky is the owner of a business supplying goods to other traders. He has just received the financial statement for his business for the year ended 31 December 2022 from his accountant. Below are the summarized financial statements:

Required:

i) Calculate for Banky each of the following ratios for the year ended 31 December 2022 (where appropriate, calculations should be approximated to two decimal places):

- Net profit margin. (2 marks)

- Return on capital employed (using the closing year-end value for capital employed) (2 marks)

- Current ratio. (2 marks)

- Liquid (acid test) ratio. (2 marks)

- Rate of inventory turnover. (2 marks)

ii) Based on the ratios calculated in i) above, and all other information provided, assess the performance (profitability) of Banky’s business. (5 marks)