Question

Answer

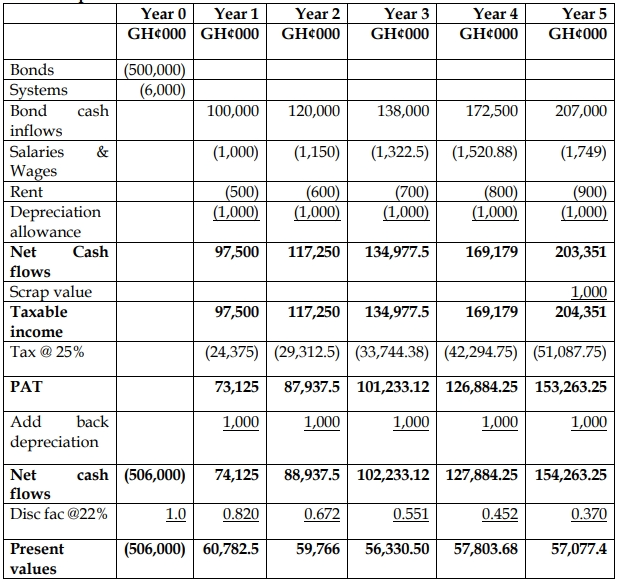

NPV = (506,000)+291,760 = (214239.9)

Decision: NPV is negative and the initiative should not be accepted.

ii) Reasons why NPV is preferred to payback period

- Considers time value of money

- considers only cash flows and not profit

- Considers cash flows after payback period

- Shows magnitude increase in shareholder value

b) Computation of RRR

Expected return = 25%

Return (r ) = rf + B(Rm – rf)

Rf = 14%

B=1.9

Rm = 14% +9% = 23%

r = 14% + 1.9 (23% -14%)

= 31.1%

Decision: Since the required return of 31.1% is higher than the expected return of

25% for project Sankofa, the project should be avoided.