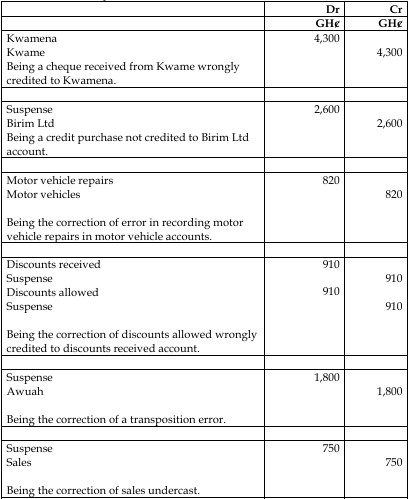

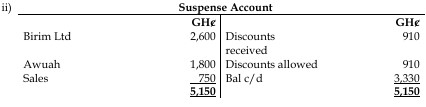

Question

Answer

iii) Uses of Suspense Account

- Suspense accounts are used when errors have made the trial balance totals disagree. It temporarily holds the difference between debits and credits until errors are identified and corrected.

- A suspense account can also be used when the bookkeeper knows the debit or credit entry for a transaction but not the corresponding entry. It acts as a placeholder until the correct entry is determined.

- The suspense account is a temporary account that is required only until the errors have been identified and corrected, allowing the business to continue producing final accounts. (4 marks)

b)

i) How Control Accounts Help in Detecting Errors

- The balance on the receivables control account should equal the balance on the schedule of receivables, and the balance on the payables control account should equal the balance on the schedule of payables. By comparing these balances, it is possible to identify that errors have been made.

- The possibility of errors in the sales ledger and purchase ledger can be reduced since they have been reconciled before inclusion in the trial balance.

- If no controls were used and the trial balance did not agree, all the accounts would need to be checked. Control accounts save time in finding errors. (3 marks)

ii) How Control Accounts Help in Preventing Fraud

- Division of duties will mean control accounts are the responsibility of more than one person.

- This makes it difficult for employees to commit fraud, as the control account acts as an independent check on the work of ledger clerks. (3 marks)