- 20 Marks

Question

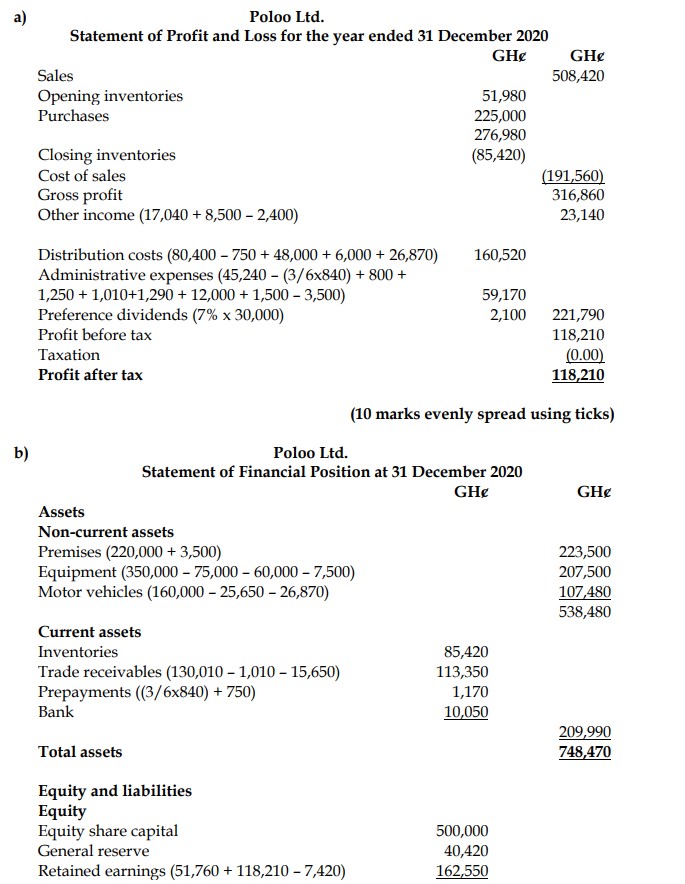

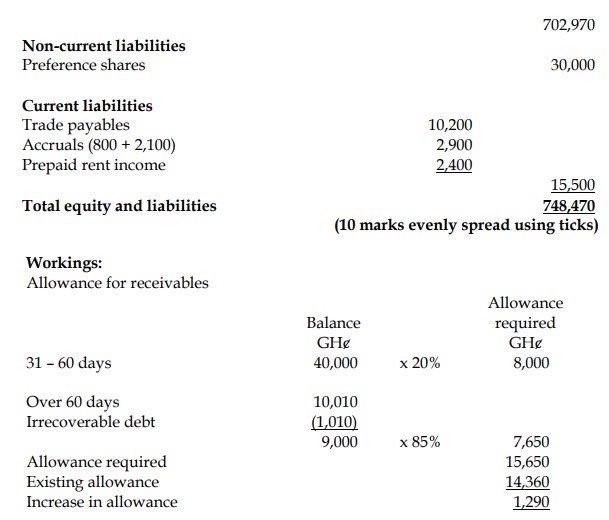

The following is the trial balance of Poloo Ltd as at 31 December 2020:

| Account | Debit (GH¢) | Credit (GH¢) |

|---|---|---|

| Authorised, issued, and called-up capital: | ||

| – 500,000 equity shares of GH¢1 each | 500,000 | |

| – 60,000 7% redeemable preference shares of 50p each | 30,000 | |

| Equipment: cost | 350,000 | |

| Equipment: accumulated depreciation | 75,000 | |

| Motor vehicle: cost | 160,000 | |

| Motor vehicle: accumulated depreciation | 25,650 | |

| Premises | 220,000 | |

| Inventory as at 1 January 2020 | 51,980 | |

| Bank | 10,050 | |

| Sales | 508,420 | |

| Purchases | 225,000 | |

| Trade receivables | 130,010 | |

| Trade payables | 10,200 | |

| Distribution costs | 80,400 | |

| Administrative expenses | 45,240 | |

| Irrecoverable debts | 1,250 | |

| Allowance for receivables | 14,360 | |

| Rent received | 8,500 | |

| Income from investments | 17,040 | |

| Interim dividend on equity shares | 7,420 | |

| Retained earnings | 51,760 | |

| General reserve | 40,420 | |

| Total | 1,281,350 | 1,281,350 |

Additional information:

i) Inventories as at 31 December 2020 are valued at GH¢85,420.

ii) Insurance includes GH¢840 for one and half years ending 30 June 2021. Insurance is included in administrative expenses.

iii) Rent received includes an amount of GH¢2,400 paid in advance as at 31 December 2020.

iv) Distribution costs of GH¢750 were prepaid, and administrative expenses of GH¢800 were owing as at 31 December 2020.

v) The total trade receivables balance of GH¢130,010 includes a balance of GH¢1,010 which has been outstanding for ten months. Poloo Ltd has decided to write off this balance.

vi) Poloo Ltd’s policy is to allow for receivables on the basis of the length of time the debt has been outstanding. The aged analysis of trade receivables at 31 December 2020 and the required allowance are shown below:

| Age of Debt | Balance (GH¢) | Allowance Required |

|---|---|---|

| 0 – 30 days | 80,000 | Nil |

| 31 – 60 days | 40,000 | 20% of balances |

| Over 60 days | 10,010 | 85% of balances |

vii) On 15 January 2020, Poloo Ltd purchased premises at a cost of GH¢105,000. This cost included GH¢3,500 relating to legal costs. The legal costs of GH¢3,500 had been included in administrative expenses and not in the cost of premises. Premises are not depreciated.

viii) On 1 April 2020, Poloo Ltd purchased equipment that cost GH¢50,000. This transaction was entered in the accounts on 1 April 2020.

ix) Depreciation is to be provided as follows:

- Equipment: 20% per annum on cost

- Motor vehicles: 20% per annum reducing balance basis

x) Depreciation on equipment is apportioned 20% to administrative expenses and 80% to distribution costs. Depreciation is charged for each month of use. Depreciation of motor vehicles is treated as a distribution cost.

Required:

Prepare, for Poloo Ltd, the following statements in accordance with International Financial Reporting Standards (IFRS):

a) Statement of Profit or Loss for the year ended 31 December 2020.

(10 marks)

b) Statement of Financial Position as at 31 December 2020.

(10 marks)

Answer

- Uploader: Theophilus