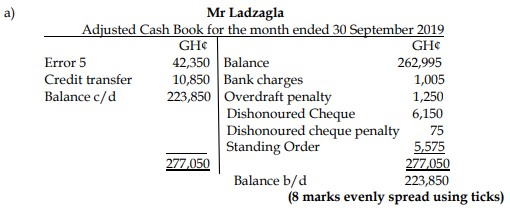

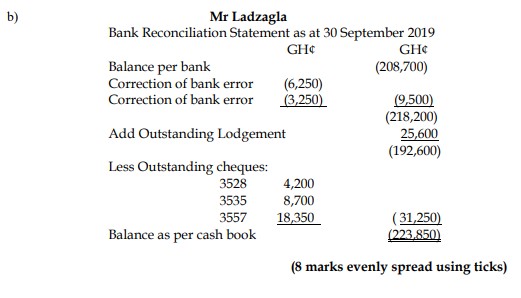

Question

Answer

c) Reasons for Preparing Bank Reconciliation on a Regular Basis

- Identification of Errors: Preparing bank reconciliations regularly helps in identifying errors made by the bank, the company, or both. For example, a business may have omitted to post receipts from receivables.

- Account for Unrecorded Transactions: Items such as bank interest, charges, standing orders, direct debits, and dishonoured cheques are often known by the bank but not identified by a business until it receives the bank statement and prepares the bank reconciliation.

(2 points well explained for 4 marks)