Question

Answer

a) Fundamental Qualitative Characteristics

Relevance:

Information must be relevant to the decision-making needs of users. Information is relevant if it can be used for predictive and/or confirmatory purposes. It has predictive value if it helps users to predict what might happen in the future and confirmatory value if it helps users confirm past predictions. Only information that is material can be relevant.

(4 marks)

Faithful Representation:

To be useful, financial information must not only represent relevant phenomena, but it must also faithfully represent the phenomena that it purports to represent in both words and numbers. A perfectly faithful representation would be complete, neutral, and free from error.

(4 marks)

b) Ledger Postings

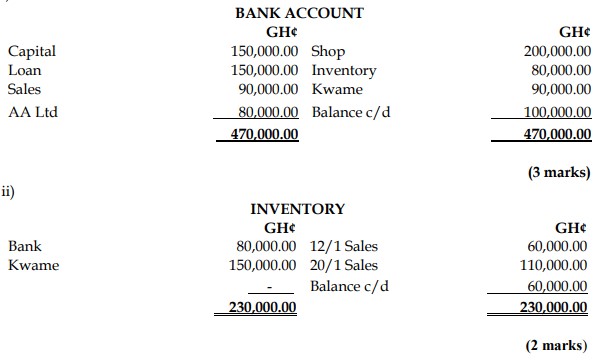

i) Bank Account

iii) Capital Account