Question

Answer

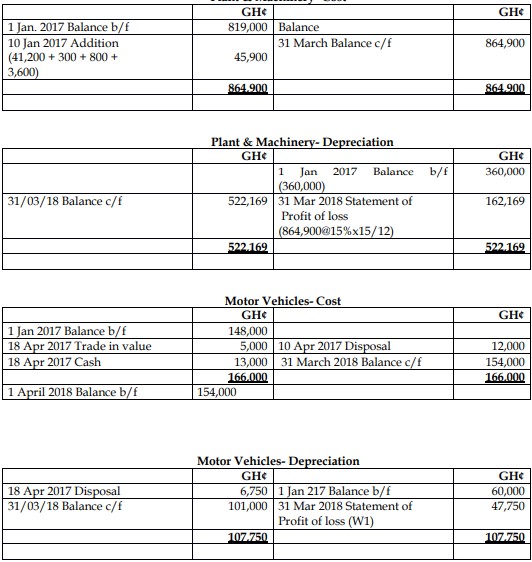

Plant & Machinery – Cost

Motor Vehicles – Disposal

Working:

Depreciation:

- (154,000 – 18,000) × 25% × 15/12 = 42,500

- 18,000 × 25% × 12/12 = 4,500

- 12,000 × 25% × 3/12 = 750

- Total = 47,750