Question

Answer

a) Assumptions underlying CVP Analysis:

- All costs can be conveniently segregated into fixed and variable elements.

- Total fixed costs remain constant while variable costs vary proportionately with the level of activity.

- The selling price per unit is given and remains constant over the relevant range of activity.

- All that is produced can be sold at the prevailing price.

- The only factor affecting costs and revenues is the volume of activity.

- Technology, production methods, and efficiency remain unchanged.

- There are no inventory level changes, or inventories are valued at marginal cost.

- There is no uncertainty.

- A single product or a constant product mix is produced and sold. (Any 5 points @ 1 mark each = 5 marks)

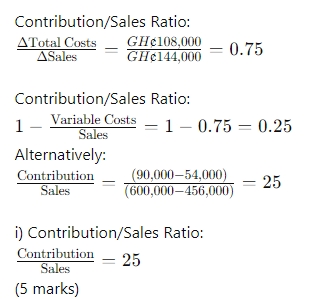

b) Workings:

| Year | Cost (GH¢) | Profit (GH¢) | Revenue (GH¢) |

|---|---|---|---|

| 2019 | 402,000 | 54,000 | 456,000 |

| 2020 | 510,000 | 90,000 | 600,000 |

| Revenue | Cost |

|---|---|

| High | 600,000 |

| Low | 456,000 |

| Change | 144,000 |

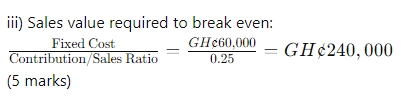

ii) Computation of Total Fixed Costs:

| Year | Revenue (GH¢) | TC (GH¢) | TVC (GH¢) | TFC (GH¢) |

|---|---|---|---|---|

| 2019 | 456,000 | 402,000 | 342,000 | 60,000 |

| 2020 | 600,000 | 510,000 | 450,000 | 60,000 |

Alternatively: Using higher sales level: Contribution = 0.25 x GH¢600,000 = GH¢150,000 Profit = contribution – FC GH¢90,000 = GH¢150,000 – FC This implies FC = GH¢60,000 (5 marks)