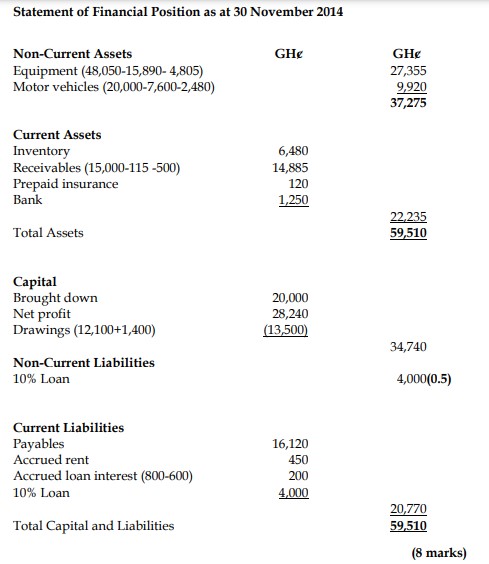

Question

Answer

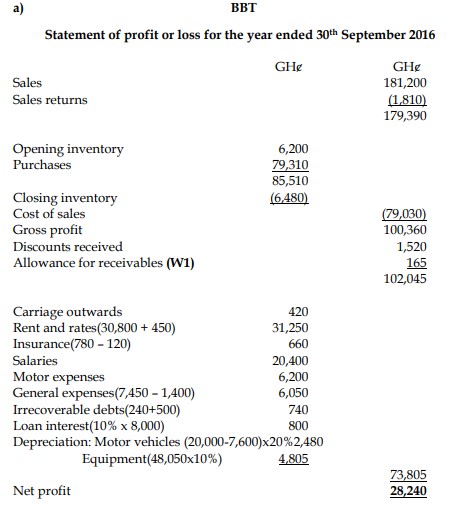

Working (W1):

Allowance for receivables: Balance b/f: 280

Provision for the year [4,000 x 1% + 2,000 x 2.5% + (1,000 – 500) x 5%]: 115

Decrease in Allowance: 165

(12 marks)