Question

Answer

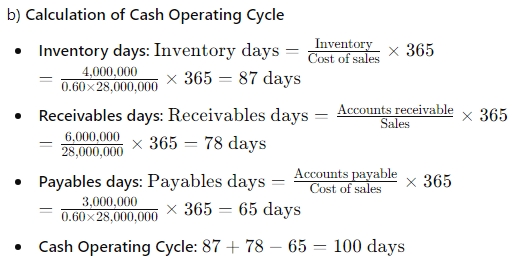

Answer:

a)

i) Cash Budget for FG Ltd (January to March 2020)

| Month | January | February | March |

|---|---|---|---|

| Receipts | |||

| Credit sales (80% previous month) | 128,000 | 128,000 | 136,000 |

| Credit sales (20% two months ago) | 30,000 | 32,000 | 32,000 |

| Total Receipts | 158,000 | 160,000 | 168,000 |

| Payments | |||

| Purchases | 42,500 | 45,000 | 47,500 |

| Labour & overheads | 71,000 | 74,000 | 76,000 |

| Machinery | – | – | 100,000 |

| Total Payments | 113,500 | 119,000 | 223,500 |

| Net Cash Flow | 44,500 | 41,000 | (55,500) |

| Opening Balance | 15,000 | 59,500 | 100,500 |

| Closing Balance | 59,500 | 100,500 | 45,000 |

| (12 marks evenly spread using ticks) |

ii) Usefulness of Cash Budgets

- Cash Flow Management: Helps in managing cash flows by providing a forecast of cash inflows and outflows, ensuring that the company has sufficient cash to meet its obligations.

- Decision Making: Assists management in making critical decisions, such as arranging for additional financing or investing surplus cash.

- Planning: Enables planning for future cash needs, such as major expenditures or expansion plans.

- Control: Provides a benchmark against which actual cash flows can be compared, allowing for monitoring and control of cash flows.

(Any 4 points for 1 mark each) (4 marks)