Question

Answer

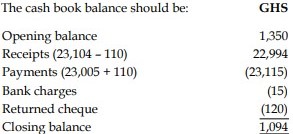

a) Adjusted Cash Book

b) Bank Reconciliation Statement as at 31st July 2015

| Description | GH¢ |

|---|---|

| Balance as per bank statement | 318 |

| Add: Banking not yet credited (GH¢1,040) | 1,040 |

| Less: Cheques drawn but not yet presented | (264) |

| Balance as per cash book (adjusted) | 1,094 |

c) Benefits of Reconciling Cash Book and Bank Statement Balances

- Error Detection and Correction: Reconciliation helps identify discrepancies such as errors in recording transactions in the cash book or the bank statement. It allows for timely correction of these errors, ensuring accurate financial reporting.

- Fraud Prevention: Regular reconciliation acts as a deterrent against fraudulent activities. Since the bank statement is an independent record prepared by the bank, discrepancies can highlight unauthorized transactions or misappropriations.

- Cash Management: Reconciliation provides a clear picture of the company’s cash position, helping in effective cash management. It ensures that all transactions are accounted for, enabling better financial planning and decision-making.