Question

Answer

a) Break-even Point (BEP): The level of sales at which total revenue equals total costs, resulting in no profit or loss. It is the point where the company covers all its fixed and variable costs.

Margin of Safety (MoS): The difference between actual or budgeted sales and the break-even sales level. It represents the extent to which sales can drop before the company incurs losses.

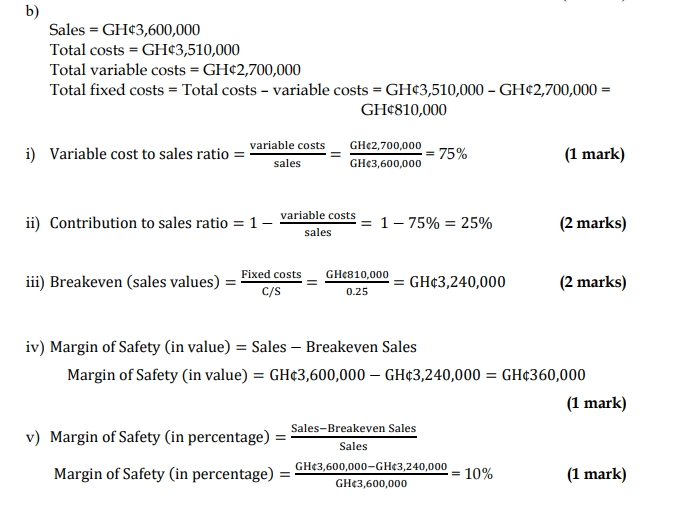

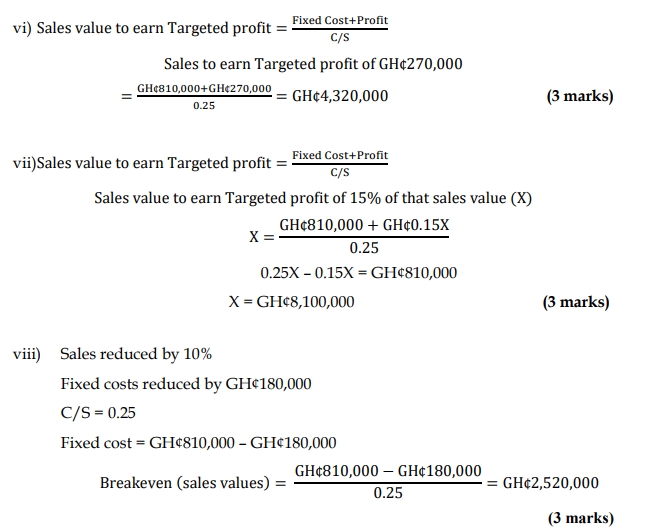

b)

| Description | Calculation | Result (GH¢) |

|---|---|---|

| Sales | 3,600,000 | |

| Total costs | 3,510,000 | |

| Variable costs | 2,700,000 | |

| Fixed costs | 3,510,000 – 2,700,000 | 810,000 |